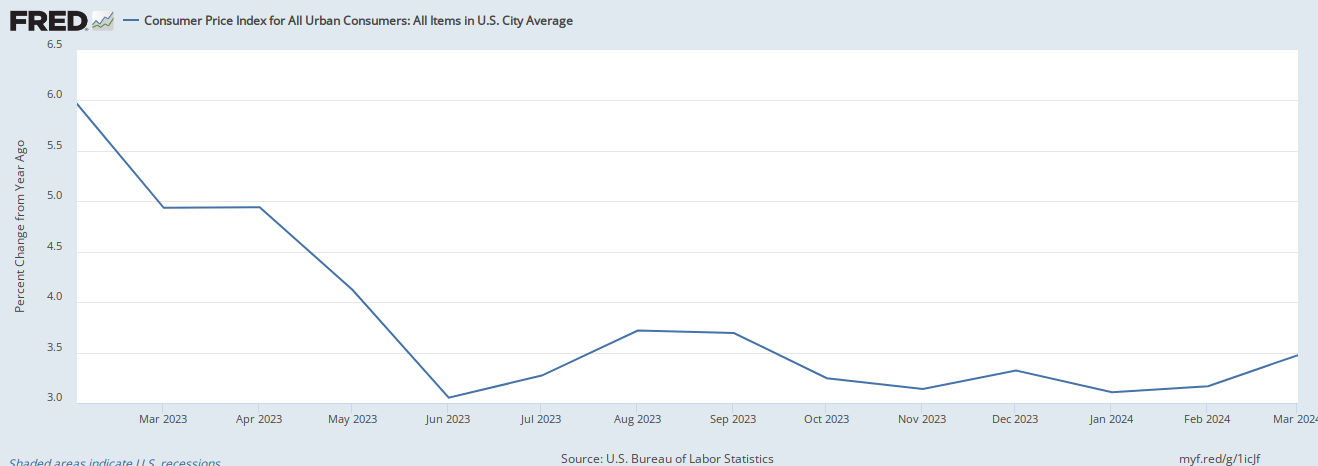

There’s been another bump in the disinflationary road. The Bureau of Labor Statistics announced the Consumer Price Index (CPI) increased 0.4 percent in February and 3.2 percent year-over-year, exceeding many economists’ predictions. That’s up slightly from January’s 0.3-percent monthly and 3.1-percent annualized increases.

Much of the increase is due to shelter and gasoline prices, which the BLS reports accounted for “over sixty percent of the monthly increase in the index for all items.” Shelter prices rose 0.4 percent last month. This is a major component of household budgets, which is why the BLS weights it at roughly 30 percent of the CPI. Gasoline gets about a 3.5 percent weight, but these prices rose 3.8 percent last month alone.

Inflation remains elevated even omitting volatile energy and food prices. Core CPI rose 0.4 percent in February and 3.8 percent year-over-year. This figure is about 0.1 percentage points lower than the January increase. Nevertheless, the past two months’ upticks in both the headline and core CPI doesn’t bode well for consumers.

What do the new inflation numbers imply about the stance of monetary policy? The Fed’s policy interest rate range is currently 5.25 to 5.50 percent. Averaging over the past three months, annualized CPI inflation is 3.6 percent. Hence the real (inflation-adjusted) Fed policy rate is 1.65 to 1.9 percent.

We need to compare this to the natural rate of interest to ascertain whether money is tight or loose. The natural rate of interest is the hypothetical, inflation-adjusted rate that balances the short-run demand for capital against its short-run supply. If the market rate equals the natural rate, the economy will produce as much as it sustainably can while avoiding accelerating inflation.

We can’t observe the natural rate of interest. But we can estimate it. The New York Fed put it somewhere between 0.73 and 1.12 percent for Q4-2023.

Market rates are above the estimates of the natural rate, implying tight money. Yet we must be cautious. Inflation has increased for two months in a row; however tight money looks now, it looked even tighter in January and February. Furthermore, as Mickey Levy notes, stronger-than-expected real growth plausibly raises the natural rate of interest (but we don’t know by how much).

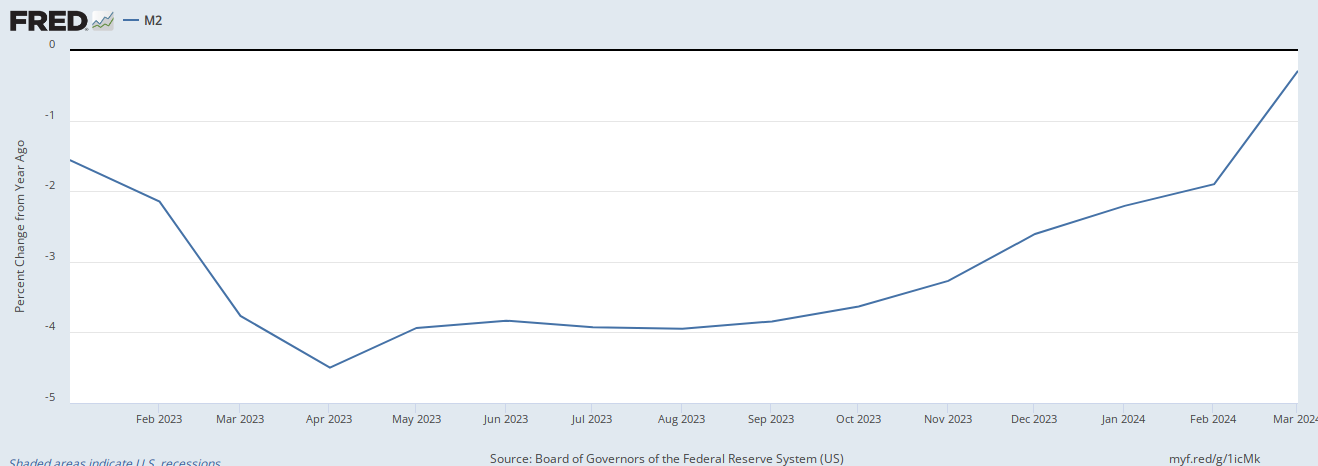

Monetary data further complicates the picture. M2 is shrinking. It’s about 2 percent lower today than a year ago. But it’s falling at an increasingly slowing rate. The Divisia monetary aggregates, which weight components based on liquidity, probably provide a more accurate picture. These are falling between 0.19 and 1.14 percent per year. But these rates, too, are not falling as quickly as in recent months. Granted, outright decreases in the money supply are highly unusual. But the rates of change imply money is becoming less tight over time.

I’ve repeatedly argued that monetary policy is too tight. That’s still my best guess — and it looks more certain using the Personal Consumption Expenditures Price Index (PCEPI), which is the Fed’s preferred measure. But I’m less confident than I was before. The question is, what does the Fed think? Fed watchers expect the Federal Open Market Committee (FMOC) will keep rates steady when it meets on March 19-20. In light of the CPI data, that’s a defensible move.

One month of higher inflation is a blip. Two months could be the start of a trend. We simply don’t know yet. The case is stronger than it was last month for the Fed to stay the course. The only thing I’m sure of is that discretionary monetary policy — steering markets by the seats of our pants — is a bad idea. But as long as the Fed insists on doing business this way, we have to offer the best advice we can. I don’t envy FOMC members. They’ll have to make a tough call next week.

{kind=link}

{kind=link}

{kind=link}