Alan Blinder thinks American households and workers have never had it so good. But because they’re trusting their lying eyes instead of experts like him, they’re disgruntled about the economy. Why don’t the hoi polloi appreciate that “unemployment is near record lows, net jobs are still being created at a breakneck pace, and inflation has fallen notably?”

There’s something fundamentally baffling about this perspective. Millions of Americans insist they confront significant material hardship, yet the commentariat — especially those who are allies of, or at least sympathetic to, the technocratic left — stubbornly doubles down on abstractions. Yes, it’s good that the unemployment rate is not higher than it is, and it is good that inflation has fallen. But it’s absurd and arrogant to insist that distant observers have a clearer picture of wellbeing than the people who say they’re hurting.

Blinder concludes that people are not satisfied with mere disinflation. “Rather, they seem to want prices for items such as gasoline and groceries to fall back to where they used to be.” He predicts (correctly, I think) that prices aren’t coming back down. Furthermore, creating deflation by engineering an aggregate demand shortfall would cause needless pain. (This isn’t true of all deflation, however. More on this below.) Amazingly, Blinder never discusses the obvious problem: The prices of goods and services have risen faster than wages for years.

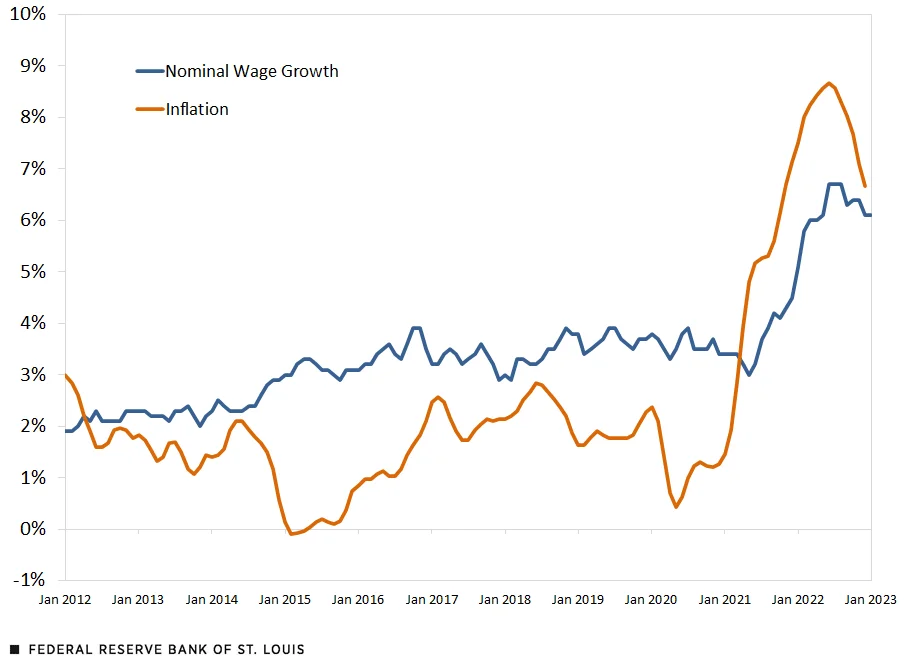

Search Blinder’s article for words such as “wage,” “salary,” and “compensation.” You won’t find them. This is an astounding oversight for an economist. The problem isn’t that things have gotten more expensive; It’s that price hikes for things we consume have outpaced our incomes. Writing for the Federal Reserve Bank of St. Louis, Victoria Gregory and Elisabeth Harding capture the problem in a revealing chart:

Contra Blinder, there’s really no puzzle here. Wages went up, but other prices went up much more. Even if both trend lines return to their pre-pandemic growth paths, workers are permanently poorer because of the real wage cuts that persisted from January 2021 until very recently.

There’s another problem with Blinder’s analysis: he thinks deflation always and everywhere causes economic harm. “It takes a truly sick economy to cause deflation,” he warns. But he’s wrong. Demand-side deflation is dangerous. Supply-side deflation, caused by improvements in technology and productive capacity, is not.

We have many historical examples of benign deflation, including the US experience for much of the late 19th century. The supply of goods and services grew faster than the supply of money, causing prices to fall. Benign deflation does not reduce output and employment. On the contrary, the increase in money’s purchasing power is a crucial signal about general productive conditions, which helps markets create as much wealth as they sustainably can.

Blinder’s analysis, in essence, is garden-variety demand-side fundamentalism. He thinks that fiscal and monetary policy can steer the economy whichever way he wants it to go, as if there are no fundamental resource constraints to limit how aggregate demand growth translates into real income growth and inflation. The past three years reveal how thoroughly falsified this paradigm is.

Blinder and his ilk can insist until they’re blue in the face that the economy is fine. Workers, families, and businesses aren’t buying it. If things were actually good, the technocratic left wouldn’t have to try so hard to convince us.

{kind=link}